Is This Home Improvement Giant a Buy Before Earnings? – November 14, 2024

The 2024 Q3 earnings season is slowly winding down, with just a small chunk of S&P 500 members yet to reveal their quarterly results. The period has so far been positive, with earnings growth remaining positive on the back of a strong showing from Technology yet again.

Below is a chart illustrating the overall earnings picture on a quarterly basis.

Image Source: Zacks Investment Research

Stay up-to-date with all quarterly releases: See Zacks Earnings Calendar.

Recently, we heard from home improvement giant Home Depot (HD – Free Report) , whose results can provide us a nice read-through of what to expect from a close peer, Lowe’s (LOW – Free Report) , in its upcoming quarterly release.

Let’s take a closer look at the HD report.

Home Depot Faces Profitability Crunch

Concerning headline figures in the release, HD posted a 4% beat relative to the Zacks Consensus EPS estimate and posted sales 2% ahead of expectations. EPS fell a modest 0.8% year-over-year, whereas sales climbed roughly 6.6% from the year-ago period.

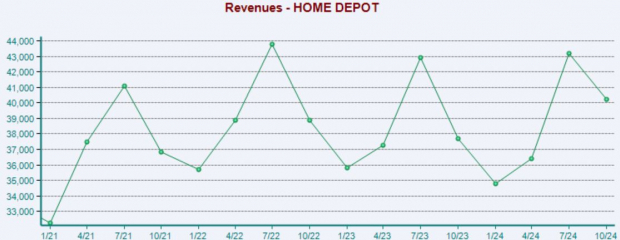

Below is a chart illustrating the company’s sales on a quarterly basis. As we can see, HD’s top line has remained stagnant over recent periods.

Image Source: Zacks Investment Research

A continued challenging operating environment impacted margins again, explaining the profitability crunch. It’s important to highlight here that the company saw increased demand stemming from recent hurricanes throughout the period, a key development that we’ll likely see in Lowe’s upcoming release as well.

The challenging environment HD has persistently noted in its quarterly releases can be attributed to a high interest-rate landscape, which has significantly affected consumers’ abilities to borrow. Many of the home-improvement projects consumers take on typically require outside financing, and the current reality just hasn’t been attractive.

In addition, housing market activity has slowed quite notably amid the high interest-rate regime, another factor that has negatively affected home improvement demand overall. The Fed’s easing cycle will help provide a big boost for the company overall, though sticky mortgage rates remain a hurdle to be cleared as well.

The company did positively update sales guidance for FY24 following the release, now expecting a decline of 2.5% year-over-year for FY24 compared to a previous range of 3 – 4% previously. Shares had a muted reaction to the release, remaining just below all-time highs.

Can Lowe’s Surprise?

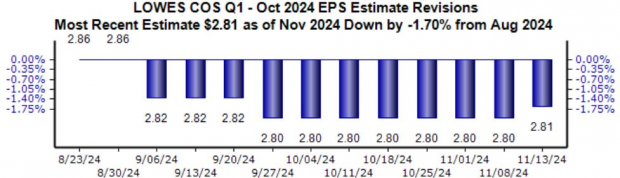

The overall setup for Lowe’s heading into its release is like that of HD, given their obvious similarities. The Zacks Consensus EPS estimate of $2.81 for the upcoming print recently saw a bump higher following the HD results, with the value reflecting an 8% pullback year-over-year.

Image Source: Zacks Investment Research

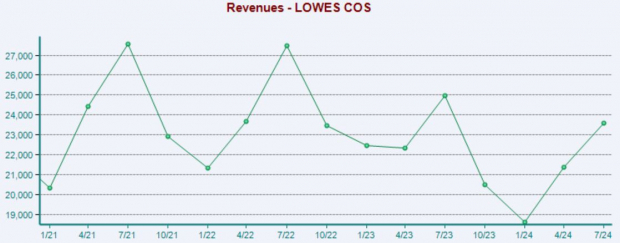

Lowe’s is also expected to see some top line weakness relative to the year-ago period, with the $19.9 billion expected 2.6% lower than the year-ago figure. The company’s overall sales trend has loosely followed that of HD, though LOW has experienced more softness over recent quarters.

Image Source: Zacks Investment Research

We’ll undoubtedly receive some commentary concerning recent storms and the current operating environment, which have undoubtedly affected Lowe’s as well. It’s worth noting here that LOW shares are just beneath all-time highs as well, but an unimpressive release will likely keep shares in a consolidating pattern.

Bottom Line

There weren’t many major surprises from Home Depot (HD – Free Report) in its latest release, with the company’s results again affected by a challenging macroeconomic environment that has suppressed profitability.

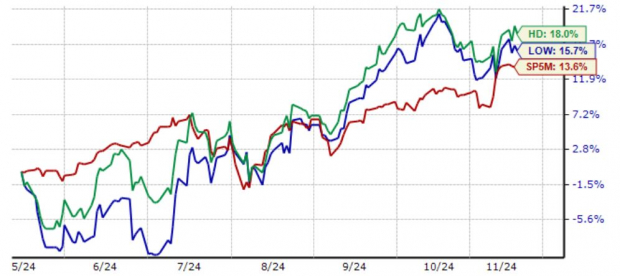

We’ll hear from a close peer, Lowe’s (LOW – Free Report) , on November 19th. The company likely faced the same issues as HD throughout the period, with sales and EPS expected to decline year-over-year. Both stocks have been notably strong over the last three months, though, outperforming the S&P 500.

Image Source: Zacks Investment Research

While profitability has been suppressed, both companies remain in a favorable spot given the Fed’s current easing cycle, likely reflected by the positive price action over the last few months.

link